Proposition 13

|

Proposition 13 is a limitation on property taxes. California voters overwhelmingly passed this legislation on June 6, 1978. Prior to 1978, real property was appraised in cycles, approximately every three to five years. This meant that every few years, each property was brought up to current market value levels. It was difficult for homeowners to predict the increases in their property taxes which made the additional costs difficult to absorb.

Except in certain instances, real property is assessed at its 1975-76 base year level and cannot be increased by more than 2% annually as mandated by State law. Real property is reassessed, however, at its current fair market value at the time a change in ownership occurs, establishing a new base year value. Similarly, the market value of any new construction is also added to assessments as of its completion date, changing the base year value. With the passage of Proposition 8, also in 1978, the Assessor is required to assess real property at the lesser of its base year value indexed by no more than 2% per year, or its current market value as of January 1st. Proposition 13 also limits the amount of taxes that can be charged to an owner of locally assessed property to 1% of the property’s taxable value, plus any voter approved bonded indebtedness, service fees, improvements bonds, and special assessments. Historically, the market value of real property has increased at a significantly greater rate than the assessed value, which is limited to no more than 2% per year, in accordance with State law, unless there is a change in ownership or new construction. The result has been a widening disparity between the market value and assessed value of property in San Luis Obispo County. Long time property owners benefit from lower assessments while newer property owners are adversely impacted by assessments that can be as much as ten times greater than that of a comparable property held by the owner for many years. |

Proposition 13 Base Year DistributionThe Base Date represents the oldest ownership interest held by the current owner(s) of record in a piece of property valued by the Assessor's office under the guidelines of Proposition 13.

|

Proposition 8

Local home values reached an all-time high in the beginning of 2006. This marked the peak of the third housing cycle since the passage of California's historic Proposition 13 in 1978. The peak was followed by months of market inactivity as homeowners continued to have hopes of receiving top dollar for their property. As overall economic conditions deteriorated, property owners failed to make mortgage and property tax payments, and property values began to fall, marking the decline phase of the housing cycle.

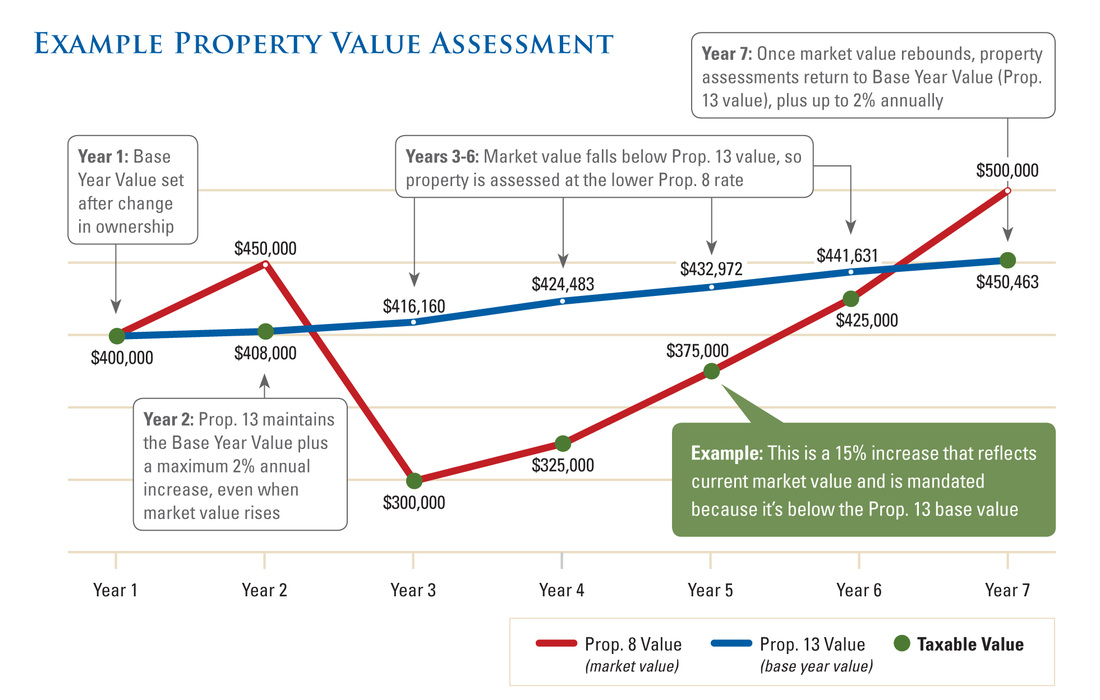

California's Proposition 13, passed in 1978, establishes the base year value for property tax assessment. It also caps the growth of a property's assessed value at no more than two percent a year unless the market value of a property falls below the base year value.

Also passed in 1978, Proposition 8 allows a property to be temporarily reassessed at a lower value. It requires that either the adjusted base year value (Prop 13 value) or the current market value determine a property's annual assessment. A decline-in-value occurs when the current market value of your property on January 1st is less than the adjusted base year value (Prop 13 value). When this occurs, the Assessor will place the market value on the assessment roll, providing relief to taxpayers. The taxpayer should always receive the lower of the Prop 13 value or the current market value as the taxable value for their property.

At the end of 2007, we began the process to proactively review residential properties within the County for potential "decline-in-value". Over 26,000 properties were reviewed that first year. In each subsequent year, as the real estate market continued to fall, these properties were reviewed with additional tax relief provided. In addition, as the market continued to drop, the Assessor continued to expand the search for potential "decline-in-value" properties to include purchase dates as early as January 1, 2001 and also income and commercial property types. This increased the number of properties reviewed to over 56,000 annually, and resulted in a cumulative countywide reduction in assessed value by more than $4.5 billion.

During 2012, real estate market conditions improved by an average of 8% countywide, with some areas increasing in value at a greater rate and some at a lesser rate. This is great news for homeowners as their home increases with market increases.

Under Proposition 13, base year values may not be increased more than two percent per year unless there is a change in ownership or new construction. However, if a property has been assessed under "decline-in-value" status, once the value of the property rises, the taxable value can increase by more than two percent a year. Increases greater than 2% could continue up to the annually adjusted base year value (Prop 13 value). When a property owner is receiving tax relief as result of a reduced assessment under a Proposition 8 "decline-in-value", the Assessor's Office is mandated to review and assess the property at market value every year until such time that the annually adjusted base year value (Prop 13 value) is once again the lower value. When that occurs, the annually adjusted base year value (Prop 13 value) is restored and the property will once again be under the maximum 2% limitation of Proposition 13. A property can never be assessed for greater than it's Prop 13 value.

The diagram below provides an illustration of the tax savings that a property owner assessed under a Proposition 8 "decline-in-value" would receive.

California's Proposition 13, passed in 1978, establishes the base year value for property tax assessment. It also caps the growth of a property's assessed value at no more than two percent a year unless the market value of a property falls below the base year value.

Also passed in 1978, Proposition 8 allows a property to be temporarily reassessed at a lower value. It requires that either the adjusted base year value (Prop 13 value) or the current market value determine a property's annual assessment. A decline-in-value occurs when the current market value of your property on January 1st is less than the adjusted base year value (Prop 13 value). When this occurs, the Assessor will place the market value on the assessment roll, providing relief to taxpayers. The taxpayer should always receive the lower of the Prop 13 value or the current market value as the taxable value for their property.

At the end of 2007, we began the process to proactively review residential properties within the County for potential "decline-in-value". Over 26,000 properties were reviewed that first year. In each subsequent year, as the real estate market continued to fall, these properties were reviewed with additional tax relief provided. In addition, as the market continued to drop, the Assessor continued to expand the search for potential "decline-in-value" properties to include purchase dates as early as January 1, 2001 and also income and commercial property types. This increased the number of properties reviewed to over 56,000 annually, and resulted in a cumulative countywide reduction in assessed value by more than $4.5 billion.

During 2012, real estate market conditions improved by an average of 8% countywide, with some areas increasing in value at a greater rate and some at a lesser rate. This is great news for homeowners as their home increases with market increases.

Under Proposition 13, base year values may not be increased more than two percent per year unless there is a change in ownership or new construction. However, if a property has been assessed under "decline-in-value" status, once the value of the property rises, the taxable value can increase by more than two percent a year. Increases greater than 2% could continue up to the annually adjusted base year value (Prop 13 value). When a property owner is receiving tax relief as result of a reduced assessment under a Proposition 8 "decline-in-value", the Assessor's Office is mandated to review and assess the property at market value every year until such time that the annually adjusted base year value (Prop 13 value) is once again the lower value. When that occurs, the annually adjusted base year value (Prop 13 value) is restored and the property will once again be under the maximum 2% limitation of Proposition 13. A property can never be assessed for greater than it's Prop 13 value.

The diagram below provides an illustration of the tax savings that a property owner assessed under a Proposition 8 "decline-in-value" would receive.

|

For more information regarding Proposition 13 and Proposition 8, watch this video featuring County Assessor, Tom J. Bordonaro, Jr. and Brad Pomerance of Charter California Edition. |

|